So This Guy Walks into a Branch…

I like to think of myself as a tech-savvy consumer, and that includes my banking habits. That means that I rarely step across the threshold of my bank’s branch, since most of what I need can be accessed online, or via my bank’s mobile app.

However, when it comes to complex interactions and larger spending decisions, I still prefer my local branch. What’s more, I have repeatedly gone back to the same bank as we have added new investments, even when they didn’t offer the best rate. Why? Because I value their expert advice, their understanding of my history, and, most importantly, their ability to see the whole picture — rather than just an isolated transaction.

Bank Customers Want It All

In this sense, I am not alone. The digitalization of banking has transformed customer expectations and behavior. Advances in technology have allowed customers like me to manage our own accounts remotely, from any place at any time. Yet for the more complex transactions, we still prefer personal interactions at our local branches.

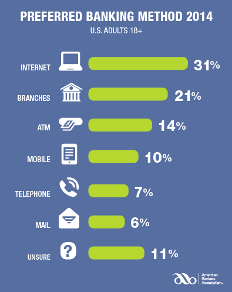

An annual survey of 1,000 U.S. adults for American Bankers Association (ABA) by Ipsos Public Affairs, in August, 2014 found that consumers are embracing mobile banking in ever-increasing numbers. However, in-person branch visits are still popular with many customers. Preference for branch banking had increased year over year from 2013, from 18 percent to 21 percent, and 89 percent of customers who come to the branch required advice for complex financial products.

An annual survey of 1,000 U.S. adults for American Bankers Association (ABA) by Ipsos Public Affairs, in August, 2014 found that consumers are embracing mobile banking in ever-increasing numbers. However, in-person branch visits are still popular with many customers. Preference for branch banking had increased year over year from 2013, from 18 percent to 21 percent, and 89 percent of customers who come to the branch required advice for complex financial products.

Today’s customers expect the best of both worlds: the convenience and easy access to online banking, along with the expert advice and personal guidance from their local branch. In short, they expect a blending of the physical and virtual, a value proposition that online-only banks cannot match.

The Branch Experience Can Either Make or Break the Business

This is not to suggest that retail banks can rest on their laurels. In a Cisco survey of 7,200 bank customers in 12 countries, 43 percent said their primary bank does not understand their individual needs. Moreover, nearly one in four bank customers intend to choose another provider (other than their primary bank) for their next financial product or service. Increasingly, that provider could be an online-only competitor such as Google or PayPal, or a retailer.

For their branches to thrive and drive differentiation from online-only banking disruptors, they need to take key steps to improve their customers’ experience. If banks continue to provide poor quality of service and undifferentiated offerings from their branch locations, they will continue to experience business erosion. The disruptive Fintechs, such as QuickenLoans.com, need only software and well trained contact center-based experts to fulfill their customers’ banking needs. Consider QuickenLoans.com success: it is the fourth largest home lender in the United States and continues to win market share.

Traditional banks must differentiate by offering a personalized, educational experience, face-to-face and in the branch. Yet a blending of the physical and virtual is critical. That brick-and-mortar experience must be seamlessly integrated with online offerings, so the branch feels like an extension of the home and mobile banking experience. Since fewer people are entering the branch, banks should view every customer visit as a golden opportunity that can’t be lost.

Compelling, engaging interactions are key to getting closer to customers and outperforming the Fintechs who struggle when it comes to building personal relationships with customers. Building the trust of the customer, and gaining insights on their personal needs not only builds loyalty, but also creates opportunities for banks to better suit the customers with additional relevant financial services.

Again, the seamless blending of virtual and physical assets offers traditional banks a clear path forward. The Cisco survey tested five concepts that focus on ways to deliver better advice (virtual financial advice, virtual mortgage advice, automated investment advice) and more valuable mobile services (branch recognition, mobile payments). Globally, 75 percent of all respondents would move their money for one or more of the five concepts. In emerging markets, interest was particularly strong. These kinds of digital experiences enable banks to offer advice and convenience at scale, reaching more customers than ever before.

I’ll Give You Five Minutes…Go!

In the movie industry it is well known that if a film does not engage its audience within the first five minutes of viewing, it will be a flop. It is not so different when a customer walks into a bank branch. If that customer is seeking advice for a complex transaction such as a home loan, and there is no qualified officer available immediately, the customer will walk, and the short window of opportunity will close. In fact, a Forrester study finds that only 30 percent of clients will ever return at a later day.

By centralizing and digitally enabling mortgage services, retail banks not only solve the problem of lack of availability of an on-site qualified officer, but they are also able to personalize the experience of that walk-in customer after they enter the branch.

Know Your Customer, and Be There When They Need You

What exactly do I mean by centralizing and digitally enabling mortgage services? Just imagine a fully immersive virtual face-to-face meeting in high-definition video made available at every branch giving walk-in customers an engaging experience with a qualified manager immediately, in real time. Virtual mortgage advisors on video and customers at the branch would instantaneously see and talk to one other on a high-resolution screen. The interaction would feel as if it were taking place in one room.

If that customer had just recently inquired about a loan online, just as soon as he or she walks in the door, Wi-Fi analytics could identify all the essential elements and stages of the transaction necessary to carry on what started as an online interaction directly into an in-person interaction, seamlessly.

Data analytics can also enable banks to match the right advisor to the right customer. By focusing on socioeconomic profiles and buying behaviors of a specific customer, the matched advisor would leverage detailed insight to drive a much richer customer engagement.

Mr. Banker, You Move Me

Today’s banking market is saturated with options, and customers are increasingly choosing the products or services of banks based on the convenience and quality of the experience. Emotions, reactions, fulfilled needs and personalized experiences become the decisive factors. By digitizing the delivery of advice, and supporting that advice with automation and analytics, retail banks can capture their customers’ devoted attention, and better yet, their loyalty. Nationwide Building Society reported recently that their customer net satisfaction rate improved 20 percent after their experience accessing a virtual mortgage assistant.

Most important, banks can return to their core area of expertise: offering advice and guidance on important financial decisions. By using innovation to engage with customers on a personal and personalized level, the brick and mortar banks will be the new disruptors in the digitized financial market place.