The mobile market continues to evolve at a blindingly fast pace. It seems as though new faster, sleeker, and more powerful mobile devices are launched every day. And new categories of mobile devices are created almost overnight. The number of applications available to run on these revolutionary new mobile devices is staggering, numbering in the millions. The insatiable demand for mobile devices and new bandwidth-hungry applications is generating enormous amounts of mobile data. The Cisco Visual Networking Index™ (Cisco VNI™) predicts that these trends will cause global mobile data traffic to increase 11-fold from 2013 to 2018, surpassing 15 exabytes per month by 2018.

In spite of this phenomenal growth and insatiable consumer demand, many MNOs are struggling to profit from this mobile gold rush. Mobile operators are watching as their average revenue per customer (ARPU) flattens or declines. Despite increasing customer appetite for mobile data, minutes of use in their cash-cow voice business are falling off sharply, and usage of text messaging is peaking. In fact, Ovum predicts that 2018 will mark the first year of revenue contraction in the history of the global mobile market. Following four years of less than 1 percent growth between 2012 and 2017, revenues will decline by 1 percent in 2018, ending the year $7.8 billion lower than in 2017.

This mobile paradox – huge growth and customer demand, yet significant business and market challenges – seems to be unique to the mobile industry. When other industries, such as the automotive industry, face healthy customer demand, they build out more capacity, sell more cars, and reap greater profits. Mobile operators need to build out more network capacity to keep up with the voracious customer demand, but they are struggling to convert these investments into higher revenues and profitability. Much of this business is being lost to substitute over-the-top (OTT) services and to major shifts in usage behaviors. Mobile consumers would rather pay for these OTT services or be subjected to advertising from the likes of Google, Facebook, YouTube, and the App Store, than pay more to mobile operators.

Not only is it a challenging world for mobile operators to be doing business in, but a number of major disruptors are radically altering the entire mobile ecosystem. The rise of software platforms (from “walled gardens” to “walled ecosystems”), the availability of new fast mobile networks, and the Internet of Everything (growth of network-connected devices) are causing significant disruption and uncertainty across the industry. Equally, the move to cloud delivery models (“everything as a service”), the changing industry structure, and the role of regulators are fundamentally changing the mobile ecosystem.

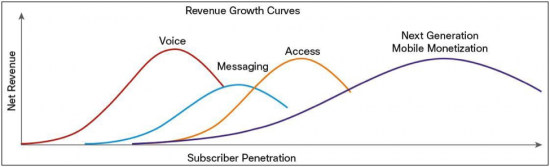

The history of the mobile industry has involved huge and successful waves of revenue growth. For a long time the mobile industry made huge sums of money from the mobile killer app – voice. However, high or unlimited minute plans and changing usage have meant the end of that growth wave. Messaging provided operators with perhaps one of the highest-margin and highest-growth products of all time, from any industry. OTT applications such as WhatsApp, Snapchat, and social media saw that revenue wave crest. Lately, MNOs are watching mobile data access rise to well over one-half of their total revenue, fueled by the insatiable consumer need to connect their mobile devices and applications. However, the crest of this third growth wave is visible on the horizon as the industry disruptors begin to shape a new mobile world.

The question for mobile operators everywhere is, what is this fourth, or next, wave of mobile growth? What are the new opportunities for them to monetize their assets and extensive investments in their mobile networks? How can MNOs continue to enjoy the success and profitability in this new mobile world that they have had in the past?

Questions to these answers can be found in our white paper: Digging for the New Mobile Gold: The Next Generation of Mobile Monetization