Today’s banking consumers are used to experiences that reflect their likes, dislikes, past histories, and even their future plans. But not always from their banks. These kinds of interactions are more common when buying an online book, streaming a movie, or planning a vacation. Despite numerous omnichannel initiatives, many banks continue to lag in providing contextual, relevant, and convenient experiences to their customers. And while many customers yearn for personalized financial guidance, a Cisco survey of 7,200 smartphone users and bank customers in 12 countries found that for too many bank customers, the choice is between no advice, or what they perceive to be generic advice delivered inconveniently.

As a result, bank customers often try to attain their most important financial goals on their own, via “friends” on social media, or from non-traditional providers of financial services. Moreover, since the financial crisis of 2007-2008, banks’ brand equity has fallen.

Our study revealed that ~28 percent of bank customers globally do not believe banks represent their best interests; nearly one in four bank customers intend to choose another provider for their next financial product or service; and four out of five customers would trust a non-bank such as Apple, PayPal, or a retailer to handle their banking needs.

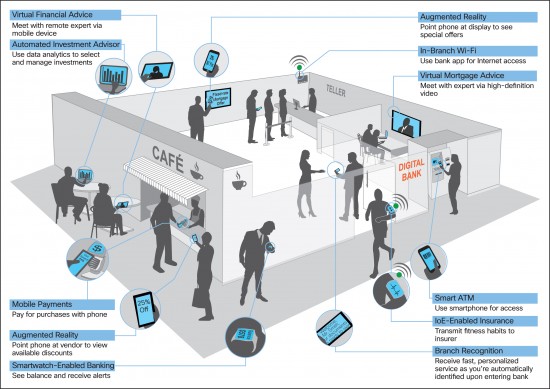

How can banks close the “value gap” with customers while regaining their trusted advisor position? The answer lies in leveraging the Internet of Everything (IoE), the networked connection of people, process, data, and things. Our research discovered high consumer interest in five IoE-enabled banking concepts that closely align to banks’ core strengths: their physical branches, financial expertise, and rich customer data.

Through the convergence of digital technologies such as mobility, analytics, and video, banks can return to what they once did best, and what set them apart: providing streamlined and secure management of transactions, combined with offering advice to guide customers’ most important financial decisions. Banks can use their size to great advantage, offering advice through a wide portfolio of offerings at scale, thereby reaching more customers, at more times, in more places, and with more relevant information than ever before.

https://www.youtube.com/watch?v=hzukF4XPMqo&feature=youtu.be&list=PLE4063C62F022E881

Despite their vast stores of customer and transaction data, many banks have failed to turn that data into actionable customer insight. The IoE solutions address this shortcoming by focusing on ways to deliver better advice (virtual financial advice, virtual mortgage advice, automated investment advice) and more valuable mobile services (branch recognition, mobile payments).

These IoE solutions resonate with customers globally; more than 60 percent would move their money (i.e., open new accounts, invest assets) to access IoE-enabled advisory services. In emerging markets, respondents are twice as likely as their counterparts in developed countries to be interested in the new banking experiences we tested.

However, to implement these solutions, banks must take the foundational step of creating frictionless interactions with their customers by moving from an archaic, paper-based approach to a fully digitized business process.

By implementing the five tested concepts, banks can realize bottom-line profit increases ranging from 5.3 percent in Germany to 15.2 percent in China (based on a bank with $5 billion in annual revenue). This is the first step for banks in capturing a much wider opportunity: Cisco estimates $1.3 trillion in IoE-related Value at Stake for the financial services industry from 2013 to 2022.

IoE-enabled solutions will enable banks to close the value gap by reaching more customers with more valuable and relevant interactions and advice than ever before—and doing it securely. As a result, banks will reconnect with customers, differentiate themselves from competitors, and compete and thrive in the Internet of Everything economy.

Thanks for your advice, your efforts is appreciated.