I recently returned from a Financial Services Summit event in China, where I discussed trends in an omnichannel delivery strategy with an audience from 30 banks. A central part of my discussion was the notion that things are not changing, they’ve already changed. Consumers across the globe have a heavy appetite for digital services.

Digital consumers across all age groups are adopting new digital behaviors at a faster pace. For example, it took one European bank 10 years to have 20 million hits per month on their website, but when they introduced their new mobile banking app, it only took 1.5 years to reach 20 million hits per month.

In a recent Internet of Everything (IoE) in Financial Services consumer study conducted by Cisco across 12 countries, we saw that in China, there is a high interest for alternative banking solutions. However, this same group of respondents (72 percent) put the branch as their first preference for opening up an account. We saw similarly high scores across Brazil, India, Russia and Mexico. The U.S. consumers came in at 60 percent.

So, what does this tell us? For one, it tells us that we need to not only evolve our mobile strategy but also see the branch as a valuable asset that is complementary to mobile and still core to any omnichannel banking delivery model.

Yes, the branch still matters. From opening up an account, to applying for a car loan or even a mortgage, there is an educational and personal interaction component to that journey. Consumers often feel that they are not fully equipped to make decisions about financial products and services alone and often seek advice and guidance from a trusted banking specialist.

With this in mind, banks are now viewing the branch as a place for interaction and not just transactions. By providing multiple channels for guidance and education with technologies such as branch recognition and video conferencing, the branch is becoming an integral digital channel with new upsell and cross sell opportunities. For example, at a Cisco-sponsored banking roundtable event in Europe, one of my colleagues asked the bankers on the panel what they considered to be their most important digital channel. He was expecting to hear something about mobility. But, not so. The first banker to respond said: “the branch is our most important digital channel.”

Many banks are still seen as technology laggards and burdened with 20th-century processes and infrastructure. This is not a viable business model for the 21st century. Banks can turn their size, physical branches, and human expertise to their favor as they offer many more customers a wide portfolio of interactive experiences and advice. By blending physical and virtual assets, banks gain a unique advantage that non-banks, or single channel financial service providers can’t deliver. As a recent Bain & Company report says about digital versus physical channels in business, “The real transformation taking place today isn’t the replacement of the one by the other; it’s the marriage of the two into combinations that create wholly new sources of value.”

As you view the branch as a digital channel, here are a few things to consider:

Introduce New Products and Services at the Pace of Customer Expectations

In the recent survey of consumers and their views on banking (referenced above), Cisco tested the appetite for Internet of Everything-led service models like branch recognition technology, wearable devices and video. For example, customers are ready to “opt-in” for branch recognition, which is a way for banks to blend the virtual experiences customers are accustomed to online with the branch experience. Once customers opt-in to a branch recognition service, the bank can identify them as they approach the branch via a mobile banking app on their smartphones. Upon entering the branch, customers would receive priority service and other benefits.

Deliver Expert Advice as Financial Products Grow in Complexity

Whether interacting with an expert in the branch or via video conferencing on a mobile device or home PC, consumers across demographics are seeking professional advice for making difficult financial decisions. The Cisco IoE in Financial Services report also looked at the types of services consumers would be most interested in receiving via virtual meetings. The research highlighted that they wanted to “see” someone who has the expertise and authority to help them with complex banking issues. Customers of all asset levels want help with their investments and financial planning. Because the costs are high, banks tend to provide in-person investment advisory and financial planning services to a small portion of their clients. Virtual meetings, however, allow banks to scale financial advice, enabling them to serve many more customers profitably, including those starting with lower asset levels.

Humanize Customer Service Through Interactive Video

Nearly three-fourths of the world’s mobile data traffic will be video by 2019. In the era of the selfie, consumers of all ages want to see and be seen, and especially when customer service is an issue. Connecting via video collaboration delivers a more personalized experience over voice alone. We are seeing examples of this with leading brands like Amazon.com’s Mayday button and the American Express live video chat feature on its iPad application, which I blogged about last summer. Both delivery models underscore how important it is to establish real-time communications with consumers at their convenience. We have also learned in working with banks around the world that just having an audio and video connection expedited to the right expert is only the beginning. Consumers reach out because they want to get something done. So screen sharing and on-screen annotations are needed. Plus, recording interactions must be accommodated and automatic. This new level of customer engagement on a mobile device as well as in the branch allows service professionals to be consultative and build trust.

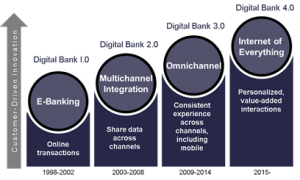

With the branch as a digital channel and integral part of delivering a customer-centric omnichannel experience, banks have an opportunity to interact with their customers and regain the loyalty and trust necessary for competing with new market entrants. As we point out in the study, we see this movement as part of the larger move, building on omnichannel strategies to taking advantage of the emerging opportunities enabled by the Internet of Everything.

Please comment and share your thoughts. This is an exciting time for banking services as personalized valued added interactions are highly valued by consumers across all age demographics.

Great article Leni. Thanks for posting it.