You order a movie online and additional suggestions pop up, based on a deep knowledge of your likes and dislikes. You plan a vacation and similar suggestions appear, reflecting your financial state, the climate in which you live (and may hope to escape for a time), and past travel history. These convenient, personalized interactions are common today — and even expected.

Yet according to a Cisco survey of 7,200 retail banking consumers in 12 countries, customer expectations for financial services are not being met. Many of the most valued customers — and not just tech-savvy Gen Y ones — feel disconnected from their financial services institutions. They state that their banks do not know them personally, and are providing advice only on the bank’s terms — in the branch, during banking hours, when staff is available, — if at all.

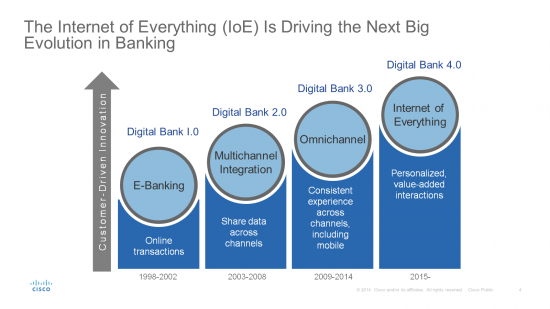

Banks understand the digital imperative, and many have made important strides with omnichannel investments, particularly in streamlining transactions across channels. Moving forward, however, they must focus their investments on the right technologies and the right customer segments.

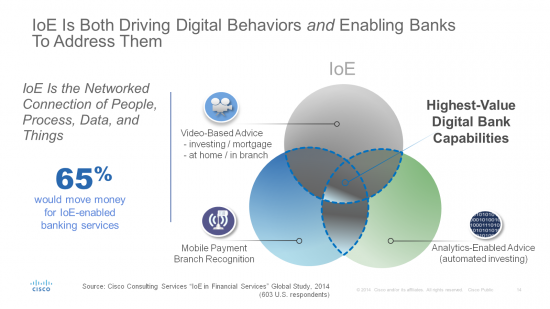

The next step of the journey is for banks to evolve the kinds of dynamic, personalized interactions that consumers now demand. Internet of Everything (IoE)-enabled solutions will be the key. IoE — the networked connection of people, process, data, and things — represents an explosion of connectivity with mobile devices leading the way. IoE is opening the door to better align with consumer behaviors and provide an environment where there is dynamic matching of customer needs and appropriate bank services in real-time, anytime – anywhere.

Cisco Consulting Services economic research estimates that by becoming as digital as its customers the upside for a typical financial services firm will be a bottom-line increase of 5.6 percent. For a financial institution with $10 billion in revenue, this represents a $392 million annual profit increase opportunity.

That is, if competitors — some from outside the traditional realm of banking — don’t fill the void first.

Here are some of the key insights from the Cisco study:

- Forty-three percent of U.S. customers believe their primary bank does not understand their needs; 31 percent feel their bank is not helping them reach their primary goals.

- The alienation of Gen Y (defined as 18- to 34-year-olds) is a concern. According to Cisco’s study, more of them make decisions alone, without any external help, than any other age group (60 percent, compared to 51 percent for all others). They are nearly twice as likely to be frustrated with their primary bank as all others (59 percent to 34 percent).

- Yet banks cannot afford to ignore other groups. The study identifies important new customer segments in terms of digital behavior — not just age. Moving forward, it will be important for banks to recognize these segments and their receptivity to interactive solutions. The study found, for example, that within Gen Y there are distinct segments looking for different kinds of engagement with their banks. And among older consumers, there are many who are more open to digital solutions than previously thought.

- What can banks do now to meet the needs of cross generation digital consumers? The people surveyed provide clear input on what they are looking for and banks can meet their needs by leveraging IoE-enabling solutions to create new experiences, particularly through:

- On-demand Advice Delivered via Video — Fifty-four percent were interested in meeting with remote financial experts via video outside a bank; another 39 percent were interested within the branch. Fifty-four percent of U.S. respondents were interested in the mortgage adviser concept, and 42 percent would likely choose a financial institution that offered this service for their next mortgage.

- Personalized Analytics — Nearly half (48 percent) of U.S. respondents were interested in receiving advice from an automated advisor that applies data analytics to personalize investing.

- Value-Added Mobile Services — Seventy-two percent were interested in using a mobile payment system that delivers their most-wanted features. For mobile payments to work, however, it is critical that they be secure. Reassurances around security and privacy were seen as the No. 1 incentive to adoption (38 percent), while fears around security were the No. 1 inhibitor (50 percent).

By leveraging these IoE-enabled solutions, banks have a very real opportunity to connect with customers and capture wallet-share. A unique value proposition arises from banks’ deep understanding of each individual’s financial needs and the ability to offer a new dimension in services and convenience. Already, we have seen banks who are embracing the opportunity realize significant increases in customer satisfaction and double-digit performance increases.

We are all consumers and we are leveraging IoE to provide convenience and value to our lives. Financial institutions have the opportunity to benefit by moving from asking “Why?” to “How” and recognizing the opportunity to bridge the gap is “Now”.

Stop by booth #4029 at BAI Retail Delivery to learn more or tweet us if you have any questions.

This is an excellent insight to learn what banks can do for your business. In order for any business to prosper, you need good banks on your side. But always keep in mind that this should not be the top priority. It’s important to build your customers especially from USA. In order to this fast, you need to buy US traffic so that people living in America visit your business website.

Here’s the direct link to a US traffic service http://traffichitz.com/buy/usa