I was on a weeklong business trip to London last month, and as I made my way to purchase a ticket for Heathrow Express train, I realized that I had left my corporate credit card at home. It was close to midnight in London, and Heathrow Express was the perfect option because I was going to stay at Hilton Paddington.

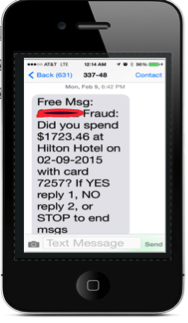

I reached the hotel rather quickly and, like always, thought to myself, “Why don’t we have something like Heathrow Express in New York?” At check-in, I offered my personal credit card and within seconds of the swipe, I received a text message from my bank:

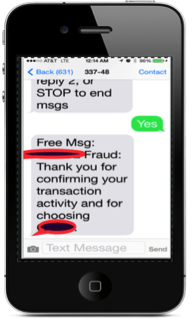

I responded in affirmative and received a confirmation. I was very impressed that my bank was looking after me.

After check-in, once I was on WiFi I launched my bank’s mobile app to make sure that I have sufficient funds to spend a week in one of the world’s most expensive cities. I wanted to take care of my mortgage payment, which was not due for another 12 days. I tried to change the effective date on the mobile app, but it didn’t work. After a couple of tries I gave up and clicked on “Contact My Bank.” The only option I had was to call, so I did:

I navigated through the regular interactive voice response (IVR) menu to reach a representative. Even though I was on the phone for more than 12 minutes, and it was a bit after midnight, the person I talked to was nice and extremely professional. She was not well versed in the mobile app, but she helped me nevertheless.

My bank’s contact center representative had no idea that I had just received a text from the bank that I was trying to make a payment on mobile app. It was irritating that I had to narrate my journey.

I wondered: what if when I was trying to contact my bank from the app, I was offered chat instead? What if the IVR experience was personalized for me when I called the bank? And, most importantly, when I reached a representative, what if she knew that I was checked into Hilton in London, that I had a point-of-sale disruption, and I was trying to pay my mortgage?

Our conversation could have gone something like this:

“Hi, Ibrahim… I see you are in London this evening. It is really late there; let me help you with your mortgage payment right away. Do you want to change the date to 2/20?”

What if my bank’s agent desktop looked like this?

It’s not science fiction. It is possible to send the holistic view of the customer journey to an agents’ desktop.

If my bank was using Cisco’s cloud-based Context Service to store customer interaction data, it could have unified all of my interaction information and provided it to the representative. It could have spared me from repeating myself.

In the example above, my bank’s representative should have known about my SMS, mobile, and self-service interactions. Even better, my bank’s representative should have known how often I call, if it is going to be a difficult interaction, and what my lifetime value to the bank is.

What other actions would you recommend agents can take to be successful and simplify both customers’ and agents’ effort?

good

good

good post

Hi Ibrahim, is this cloud context service or cacc?

Hi Mark, I was thinking about Context Service but it could be CACC or both. It depends on the use case..

At the Unified Desktop, I like to see the “Recommended Action” in the snapshot you provided. I would also like agents to have a tool that helps them identify possible adjacent issues that you might experience based on your current issue. If they addressed those issues now, it might save you from having to call back in the near future–ultimately giving them a true First Contact Resolution (FCR).

Jeff, the way Cisco Context Service is designed, it’s very easy to integrate in apps that can do as you suggest. Chris

See below, Jeff

This is so cool, I need to read up on this, thanks for sharing!

Good Post, thanks Ibrahim!