By Henky Agusleo, Vertical Manager, and Neeraj Arora, Director, IBSG Service Provider –

By Henky Agusleo, Vertical Manager, and Neeraj Arora, Director, IBSG Service Provider –  Singapore

Singapore

A rapidly expanding, tech-savvy middle class is driving an explosion of connected mobile devices, with close to a billion smartphones and tablets in the world today. These users are looking for new cloud-based “Connected Life” experiences from their mobile devices, creating tremendous opportunities for service providers (SPs). The key is in mobile cloud. The Cisco® Internet Business Solutions Group (IBSG) projects a direct worldwide mobile-cloud service opportunity of more than $60 billion by 2016, with an additional cloud pull-through market of $335 billion.

But so far, service providers have not taken the lead in offering cloud-based Connected Life services. That claim belongs to over-the-top (OTT) application developers, content providers, and device manufacturers, such as Google and Apple, who have moved quickly to take the high ground in this market.

OTTs Have First-Mover Advantage

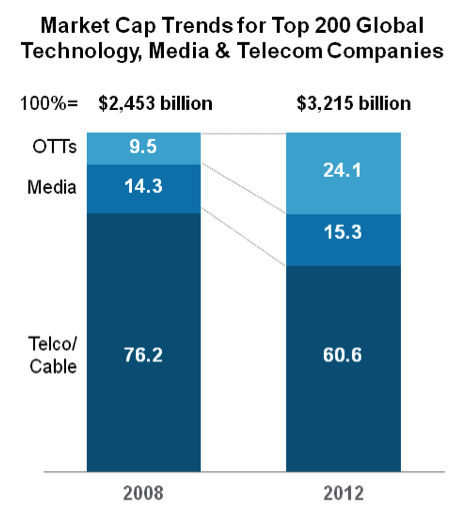

This first-mover advantage has enabled OTTs to shape new markets through mobile cloud service innovation, gain greater control in the overall mobile cloud ecosystem, and generate high market valuations. As evidence of SPs’ lost opportunity, between 2008 and 2012, SPs’ share of the combined market capitalization for the top 200 technology, media, and telecommunications companies shrank by more than 16 percent, to 60.6 percent, while OTTs increased their market capitalization share from 9.5 percent to 24.1 percent (see Figure 1).

Today, a few breakaway SPs—including NTT DOCOMO, China Mobile, Verizon, and AT&T—are beginning to realize the value in offering mobile cloud services through their own app stores or through links to outside app stores. Overall, however, SPs are still behind the curve for this crucial opportunity. Clearly, service providers must rise up to the challenge of mobile cloud to more fully realize this crucial avenue for profitable growth and higher valuations.

Figure 1. Telecom Providers Losing Market Valuation to Over-the-Top Service Providers.

Note: Telcos include AT&T, Verizon, Vodafone, NTT DOCOMO. Media include Comcast, Time Warner. OTTs include Amazon, eBay, Google, LinkedIn.

Note: Telcos include AT&T, Verizon, Vodafone, NTT DOCOMO. Media include Comcast, Time Warner. OTTs include Amazon, eBay, Google, LinkedIn.

Source: Company financial reports; Cisco IBSG analysis, 2013

One reason for the current lag is that, initially, mobile cloud services offer lower margins than traditional SP mainstays such as voice and short message services (SMS). Mobile operators who already have solid margins are reluctant to warm up to new offerings. However, to reap significant future benefits, SPs must take the long view and embrace innovations that challenge the comfortable status quo.

Revenue and Cost Levers Can Help SPs Claim the Mobile Cloud

Cisco IBSG believes that every dollar invested in mobile cloud services can bring up to seven dollars in return. To win this benefit, SPs will need to utilize value levers to increase revenues, reduce costs, and improve profitability. We have identified several specific actions SPs can take:

- Proactively manage pricing to enhance subscription revenue by moving to tiered and capped pricing, by pricing to customer value, and by lowering access costs to increase cloud service adoption.

- Leverage Big Data analyticsto increase advertising revenue, through personalization, context, and location awareness.

- Use virtualizationto optimize data-center costs, improve efficiencies, and take advantage of economies of scale.

- Optimize content delivery networks and local caching to reduce IP transport costs, manage OTT traffic, and improve quality of service.

- Leverage Wi-Fito offset incremental 3G / 4G investments and generate new revenue streams.

- Deploy “thin-client” cloud-based devicesto reduce device subsidies and customer acquisition costs.

- Partner with media companies, content providers, application developers—and even OTTs themselves—to complement their core competencies with the capabilities SPs can provide to offer full-value cloud services.

For many SPs, the road to mobile cloud success is just beginning. But a vast opportunity awaits SPs who venture into the mobile cloud. The time to reclaim the high ground is now.

To read a complete analysis of how SPs can successfully compete in the mobile cloud arena, see our white paper, “The Road to Cloud Nine: How Service Providers Can Monetize Consumer Mobile Cloud.”