Technology has and will continue to be a key enabler across every product delivery channel within the financial services sector. You simply need to explore some of the newer bank branches, available applications within app stores or investigate online innovations inherent in many institutions’ web presence to see how engrained technology has become in the customer experience. While firms are making this transition in differentiated form factors and across different channels, the trend itself is clear and pervasive; underpinned by the “anywhere, anytime” mantra and the continued consumerization of technology.

These channel developments cut across all products, but all have one common element – enabling improved and increased collaboration between institutions, their clients, businesses and/or consumers to drive accretive revenue. While these developments have and will continue to deliver impressive initial returns, they are largely siloed by either a business unit and/or delivery channel. The true potential value can only be unlocked by enabling a seamless and contextual integration of the physical, direct and mobile channels – the evolution from multi-channel to omnichannel.

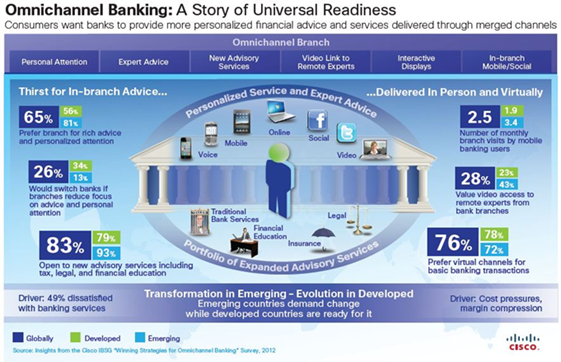

The omnichannel model enables the customer to choose how and by what method they want to conduct their business, be that in person, via a mobile device, from the home, online or with telephony. Cisco’s IBSG team has published a white paper that looks into the transformation of institutions from multi-channel to omnichannel. While the method of communication is important, the true differentiator in transformational channel evolution is the ability to integrate interaction. Institutions must be aware of the context and outcomes of customer interactions as customers move from channel to channel, product to product, or business line to business line.

From an institutional point of view, the value in the omnichannel impacts multiple factors. The opportunity for true cross-sell opportunity is enabled by providing not only expertise but contextual customer data to any channel across any product including the ability to handle a “warm” transfer across multiple channels. In addition, the customer experience is enriched by ensuring customer interactions and outcomes across institutions’ external touch points are transferred across entry points. Finally, the omnichannel model provides compelling cost savings through increased ability to leverage expertise across the corporate footprint.

Customers want more personalized, higher-quality interactions enabled by video and specialty branches that are advice-centered. The infographic below outlines customer desire for this digital change. Cisco’s Jason Bettinger, Vertical Lead, Retail Banking, discusses in a recent blog how banks specifically are differentiating the customer experience through an omnichannel approach. The development of an omnichannel branch allows collaboration across multiple technology stacks, principally applications, network and collaboration.

Source: Cisco IBSG, 2012

While the concept of an omnichannel strategy cuts across virtually all verticals within the financial services sector, examples are often most illustrative of the power.

From a customer perspective, whether you’re shopping for insurance, looking for a mortgage rate through a bank, or wanting to invest dividends from your 401k, Cisco can enable rich collaboration on any channel, on any device and it’s a sustainable experience with a consistent look and feel across multiple devices.

In the case of someone who is shopping for an insurance policy that meets their needs, Cisco can help prospective customers connect directly with agents via face-to-face video interaction from any device whether it’s a PC, tablet or smartphone. By providing customers access to the online world and offering the ability to utilize remote expert video conferencing, insurers are helping differentiate customer services and experience.

For the individual who receives a 401K distribution, they may begin looking for investment options. Through the omnichannel solution structure, that customer has the ability to connect with their financial advisor and various experts via a video chat session, across any mobile device, with seamless transition between their preferred devices. If the customer has concerns about the market changes, Cisco’s collaboration solution allows them to connect virtually with their financial advisor no matter their location.

A customer looking to conduct a mortgage transaction may need guidance on whether to go with a fixed or variable rate, in which case they can connect with a mortgage expert directly at a retail bank branch, regardless of the expert’s location. Branches can create customized online/mobile portals based on the customers’ home branch in order to provide local offers and allow contact center specialists to deliver more personalized service.

As you can see, customers will begin to experience more personalized services while still having access to expert advice, regardless of location. Technology is no longer an afterthought to retail banking and financial services alike; it is quickly becoming a staple in how institutions conduct business with their customers across all channels. Omnichannel is no longer an idea, but a solution that is meeting the individual needs of financial customers around the world.

Omnichannel is definitely part of the customer experience trends across multiple industries including financial service. Cisco just released a new chapter of the Cisco Connected Customer Experience Report outlining consumer and business trends on seamless customer experience. The press release is located here http://newsroom.cisco.com/release/1174098 and you can visit the Cisco Connected Customer Experience at http://www.cisco.com/go/customerexperience