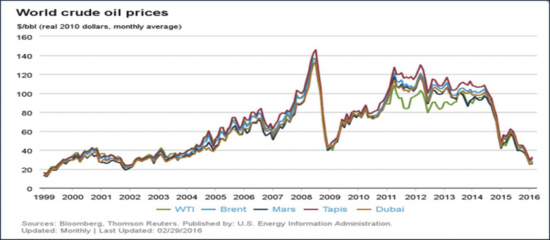

In my role as Global Manager, Energy Market, I have seen changes due to threats like the shortage of expertise and falling oil prices. The current price for crude oil is at the lowest level in two decades (U.S. Energy Information Administration). Does this mean that there are no changes and opportunities? Definitely not, when one door closes a few others open. Let’s explore some of those opening doors.

The landscape of the Oil & Gas market is traditionally categorized in three areas:

- Upstream – exploration, development, and production of O&G

- Midstream – the storage and transportation of O&G

- Downstream – processing and selling the final products

It is clear that with the current low oil price, only those oilfields where the oil can be extracted for less cost per barrel than the current selling price are still financially attractive to explore.

Upstream is a difficult place to be at this moment. Nobody wants to be the first to stop producing because others will take over your market share. Oilfields will keep producing and store the oil or take the loss for a relative short time. This leads to the current overproduction of crude oil.

With the current oil price, upstream companies would be wise to not sell more crude oil (unless it serves a strategic goal) since this can cause a further price drop.

Upstream O&G companies should focus on cost reduction in the current economic climate.

If you can sell the same amount of product while making lower costs, your margins will improve. For upstream O&G, Cisco is focusing on solutions to cut costs by becoming more efficient and effective. In the next blog, I will highlight some of the solutions which can be deployed to achieve this.

These solutions will enable better and faster decisions, prevent and shorten unplanned downtime, and provide better security and safety. All these solutions will add to the bottom line – either by increasing revenues, reducing costs, mitigating risks, and increasing customer loyalty.

Whereas upstream is challenging, midstream and downstream companies are benefiting from low oil prices as there has never been so much crude oil to store, transport, and process. Terminal companies see their storage tanks filled to the brim and pipeline companies have a lot of oil to transport. Since the price of oil is a ‘cost of goods’ for a refinery, low oil prices mean that the margins of refineries are healthier and more investments are being made in refinery land.

In the next blog we’ll explore how we’re helping profits flow for O&G companies using digital technologies.

To take a deeper dive into these macro-economic developments, read our latest whitepaper “A New Reality for Oil & Gas” and visit www.cisco.com/go/oilandgas for the latest updates.

Good to see you posting. You may wish to elaborate that large debt forces an oil firm to produce more even if it is cost inefficient adding to price volatility. Also getting faster information flow on oil production is an area where Cisco adds value. Looking forward to more articles from you.

Hi Jonathan,

Thanks for your comment.

Indeed the whole issue around large debts of the oil producers forcing them to continue to produce oil is another element of the current situation. Also Iran getting back on line to the production levels before the trade embargo, countries like Venezuela who have based their national budgets on a $110 oil price, and the fight to remain market share are all contributing to the fact that supply is higher than demand at the moment.

It will be interesting to see how this develops going forward!

Very interesting. Is there any partner in Iraq?