I wrote in my last post about the industry move to software subscription buying models. While the benefits to software companies and customers are clear, there are also many misconceptions about how this transition will happen.

It won’t take place with the flip of a switch. As customers do with any new technology or new way of doing business, they will need a smooth path to transform how they buy and consume software.

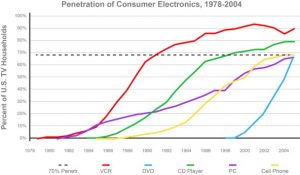

As we’ve seen with nearly every technology driven consumption transition, there remains a long tail of legacy buying. Indeed, while the pace of change has increased, it remains a multi-year journey before we see greater than 50 percent penetration. Even the DVD, which the chart below shows had one of the fastest technology adoption curves in history, took around five years to pass 50% penetration.

Source: Consumer Electronics Association eBrain Market Research

We’re seeing the same long-tail effect in the adoption of –aaS and subscription buying models as they overtake traditional perpetual and premise-based models.

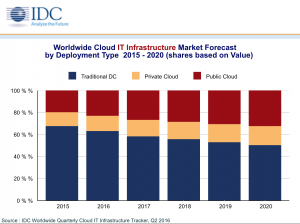

You can see from this forecast by IDC, that IT infrastructure-as-a-Service (delivered by the cloud) is expected to surpass traditional models by 2019—yet when you adjust for private cloud impact (most of which will continue to be priced and licensed in a traditional model), we won’t see greater than 50% penetration until beyond 2021.

Another misconception is that subscription buying takes place subscription by subscription, user by user, without a cross-enterprise strategy or governance. While it is true that users of these new services will find subscriptions easier to adopt because they can simply buy directly through the line of business without going through procurement—the reality is that enterprises are increasingly managing these subscriptions on a more concerted and organized basis.

In fact, most companies will need to use multiple buying models to meet the requirements of different applications and parts of the business. The overall environment might be slightly more complex during the transition, and over time, adoption of these new services will be more tightly coordinated and managed.

Leading software companies need to maintain a range of software buying and delivery models to meet customer requirements and smoothly facilitate the transition. We see this happening not through a single subscription or licensing agreement, but by way of a comprehensive licensing platform that goes across all the various consumption and delivery models customers are looking for.

As a recent report on Software Pricing Trends by PricewaterhouseCoopers observes:

Vendors must begin thinking of their application portfolios as flexible platforms that allow customers to choose among software components and pricing models.

At Cisco, we’re looking at new ways of offering a cross-architectural Enterprise Licensing Agreement that provides customers subscription on-premise, perpetual-on-premise, and in many situations, the easy movement of technologies between buying and consumption models.

I’m looking forward to telling you more about it here soon.

John