By Henky Agusleo, Vertical Manager, and Neeraj Arora, Director, IBSG Service Provider

By Henky Agusleo, Vertical Manager, and Neeraj Arora, Director, IBSG Service Provider

With nearly a billion smartphones and tablets in use today, the time is ripe for service providers (SPs) to invest in cloud-based Connected Life services for mobile devices. The Cisco® Internet Business Solutions Group (IBSG) projects a direct mobile cloud service opportunity of more than $60 billion worldwide by 2016. So far, the first-mover advantage has gone to over-the-top (OTT) players such as Google, and device makers such as Apple. However, service providers (SPs) are well positioned to capture significant revenue in the growing market for cloud-based mobile services. With the right investment and implementation strategies, they can more fully realize this crucial avenue for growth and cost savings.

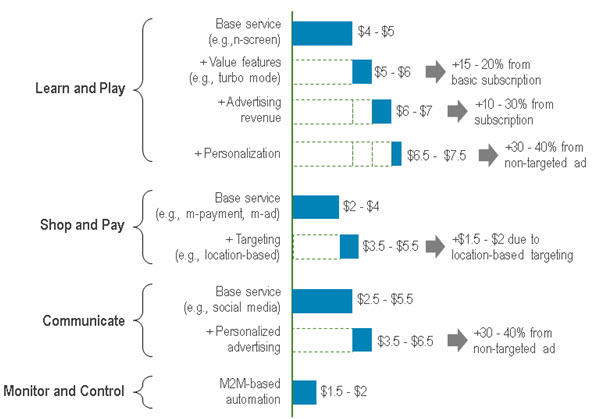

Cisco IBSG sees consumers demanding mobile-cloud services that fall into four key categories:

- Learn and Play: Gaming, video, information, productivity-enhancing services

- Communicate: Video calls, social networking

- Shop and Pay: Payments, healthcare, travel, location, context-based ads, mobile retail

- Monitor and Control: Home automation, surveillance

Sevenfold Revenue Return on Investment

Despite the $60 billion opportunity, mobile operators have been slow to make the investment necessary to develop these cloud-based services. One reason for this lag could be concern about profit margins, which tend to be significantly lower than for traditional mobile services. A number of factors could explain the lower profit margins, including:

- Use of expensive but spectrally efficient 4G/LTE networks to accommodate the ever-increasing need for broadband

- Lack of sophistication in the pricing of new services, which leads to subpar margins

- A dearth of personalized advertisements (or absence of advertising strategy altogether), which limits an SP’s ability to charge more for its advertising inventories

Service providers need to develop strategies to counter these hurdles. To help them do so, Cisco IBSG has identified several revenue and cost levers that can be used to improve profitability. Some specific levers — including subscription revenue, advertising, and personalization backed by analytics — can grow revenues up to 40 percent, while others —including data center, IP transport, mobile access, and customer acquisition — can cut costs as much as 20 percent. By implementing these levers, service providers can unlock the value of their investment in enhanced mobile cloud services and become more competitive with the OTTs that have tried to claim this territory.

The power of the revenue levers is shown in Figure 1. Based on our own research and customer engagements, Cisco IBSG has found that every $1 invested in mobile cloud services can result in up to $7 in revenue.

Figure 1. For SPs, Mobile-Cloud Services Bring up to $7 in Revenue Per Dollar Invested.

Note: Based on direct investment by major SPs for add-on services (excluding broadband access investment).

Source: Cisco IBSG, 2012

By investing in new capabilities, service providers capture additional revenue, not only through the base subscription or transactional revenue from the mobile cloud service itself, but also through value-added features that increase advertising revenue potential or boost consumer spending. These capabilities might include turbo-mode broadband services, personalization, or location-based services. We also estimate that average earnings-before-interest-and-tax (EBIT) margins of these services can be improved to up to 30 percent by applying the revenue and cost levers mentioned above. By using these levers to address their profitability concerns, SPs can in turn make the necessary investment to unlock the $60 billion opportunity.

While the opportunity is available globally, it is perhaps even more pressing for SPs in emerging markets, where demand for these mobile cloud services is being driven by a growing base of middle-class consumers. Unlike their aging middle-class counterparts in the developed world, the fast-expanding middle class in developing markets tends to be young and tech-savvy.

Next Steps for SPs

SPs should start now to develop strategies to exploit the opportunities of mobile cloud and to deliver new services that will transform the way consumers learn and play, communicate, shop and pay, and control and monitor their day-to-day activities.

To read our complete analysis of the actions SPs can take to find revenue and profitability in mobile cloud, please download our white paper, “The Road to ‘Cloud Nine’: How Service Providers Can Monetize Consumer Mobile Cloud.”