Do you feel a bit lost when people refer to certain environmental sustainability topics and aren’t sure where to start when it comes to learning more? Sustainability 101 is a blog series that you can turn to for information about different environmental terms that may come up at work, during discussions with friends, and even at your annual holiday gathering.

According to the Intergovernmental Panel on Climate Change (IPCC), climate science says we must limit warming to no more than 1.5 °C above pre-industrial levels to avoid the worst impacts of climate change. And, according to the Science Based Targets initiative (SBTi), “In order to limit warming to 1.5°C and avoid the worst effects of climate breakdown, global emissions must be halved by 2030.” To help reduce greenhouse gas (GHG) emissions, many companies are trying to figure out what their carbon footprint is so they can start making changes.

Carbon accounting, or GHG accounting, is the process in which an organization estimates the total amount of GHG emissions that are generated through its activities within a set of boundaries. The predominant standard used to guide these estimations is the GHG Protocol Corporate Accounting and Reporting Standard, first launched in 2001. The GHG Protocol establishes comprehensive global standardized frameworks to measure and manage GHG emissions from private and public sector operations, value chains and mitigation actions.

Defining and quantifying GHG emissions

GHGs were first defined in 1997, under the Kyoto Protocol, and were limited to a set of six individual GHGs or classes of GHGs: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphur hexafluoride (SF6). Nitrogen trifluoride (NF3) was added later for a total of seven gases that organizations following the GHG Protocol Corporate Accounting and Reporting Standard report on.(1)

The defined standards set through the GHG Protocol are important because they give companies the same standard to follow when they report on emissions. This in turn makes it easier for people to compare companies’ performance.

In general, GHGs are reported in units of carbon dioxide equivalents or CO2e. CO2e is a way of combining the seven gases into one unit, by looking at their effects on our environment over 100 years. If you think of GHGs as a currency, think of CO2e as being the one currency everyone uses, and you can swap currencies based on their exchange rate or so-called “emission factors”. Emission factors allow us to convert various activity data into GHG emissions and combine them into our one unit, CO2e.

As an example, if you consumed 100 kWh of electricity, to estimate the emissions you would multiply that data by your emission factor. If we used the 2023 emission factors from the United States Environmental Protection Agency (EPA), we would multiply the 100 kWh by 0.386 kg CO2e/kWh which means you would generate 38.6 kg CO2e.

As a reminder, emissions of organizations are classified into 3 scopes:

- Scope 1: Direct emissions from operations owned by the company. Examples: Heating fuel used in company buildings, fuel use in company vehicles

- Scope 2: Indirect emissions from the generation of purchased electricity, steam, heating and cooling. Example: Electricity used in company buildings

- Scope 3: All other indirect emissions that occur in a company’s value chain. Examples: Employee business travel and commuting, supplier emissions, emissions from transportation and distribution of product, emissions from use of sold products

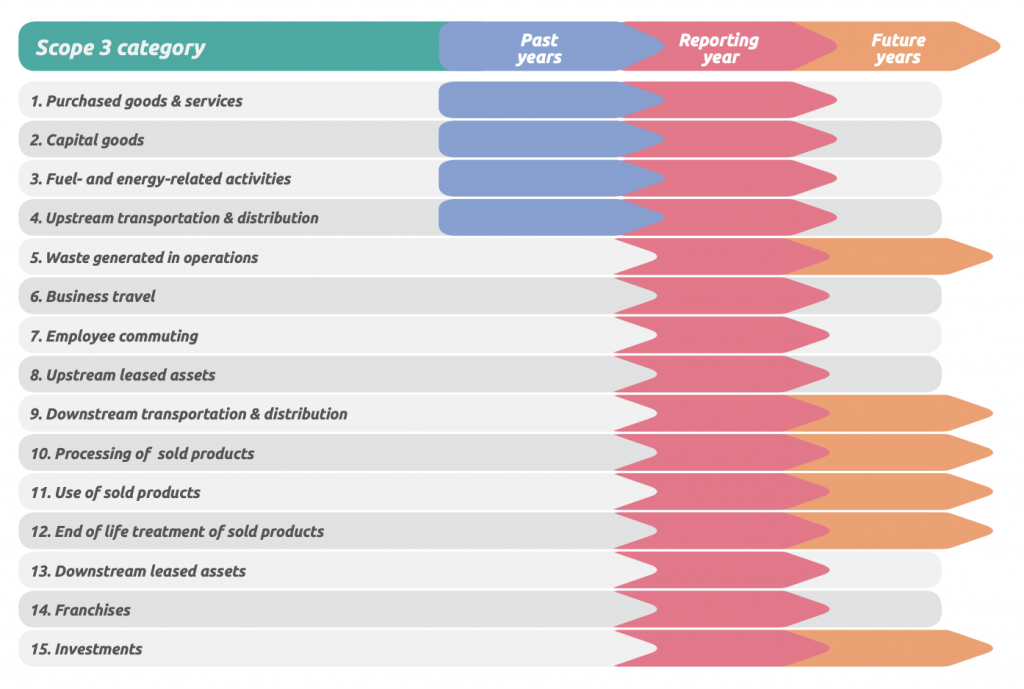

Prior to quantifying an organization’s GHG emissions, it’s important to understand the time boundaries reported on across the Scope 1, 2 and 3 inventory per the GHG Protocol. While Scopes 1 and 2 look at emissions from the reporting year, categories in Scope 3 can look at past, present, or future years as outlined in Figure 1 from a GHG Protocol report.(2) The GHG Protocol takes a lifecycle perspective, which means for certain categories, like “Scope 3, Category 11: Use of Sold Products,” an organization accounts for all of a product’s lifetime emissions in the year it’s sold.

Estimating GHG emissions

Carbon accounting is based on estimations. In general, there are three primary methods of estimating GHG emissions: Activity based, spend based or a hybrid approach that uses both.

Activity-based: Emissions are estimated by collecting primary data and multiplying the value by the relevant emission factors. Examples of primary data include energy or fuel consumed or amount of material purchased.

It can also be estimated from secondary data, which is data that is not from specific activities within a company’s value chain. Some examples include average data, proxy data or industry average data.(1)

Spend-based: Emissions are estimated by determining the amount of money spent on an activity and multiplying the value by the relevant secondary data emission factors. Emissions factors can be from an environmentally-extended input output (EEIO) database, or they can be more supplier specific, based on reported emissions and revenue information. (1)

Hybrid: Emissions are estimated by first following the activity-based approach and then using the spend based approach if there are gaps. This increases the coverage of the potential in-scope emissions sources. (1)

Improving our data

One of the goals of GHG accounting is to use primary data as much as possible, but it’s not always easy to access that data. For Scope 1 and 2, primary data is typically available, but in Scope 3, an organization is often reliant on secondary data. This can be a challenge when trying to understand how various investments or design choices are helping to reduce GHG emissions.

Cisco has set a goal to reach net zero GHG emissions across our value chain (Scopes 1, 2, and 3) by 2040, and we have also identified two near-term targets on the way to that larger goal. We are continually working to improve our data, provide accurate emissions estimates and drive GHG emission reductions.

Information regarding Cisco’s environmental, social, and governance (ESG) initiatives, goals and commitments, our latest impact, as well as policies and additional disclosures for specialized audiences, can be found in our 2022 Cisco Purpose Report and supplemental information in our ESG Reporting Hub.

1 Greenhouse Gas Protocol – Technical Guidance or Calculating Scope 3 Emissions (PDF, pp. 14, 17, 21)

2 Greenhouse Gas Protocol – Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF, p. 33)

Great blog

This is an excellent summary of carbon accounting. I will use it (with attribution) as a reference.

With thanks.

Brilliant article!

Cisco’s goal to reach net zero GHG emissions by 2040 is totally unrealistic. Because, as you say, you rely on secondary sources for Scope 3. By 2040, electricity itself will not be 100% renewable, it is a fact (it is right now 60% produced by fossil fuel in the USA. So unless you do business producing all you electricity, you raw materials, your physical distribution network and so on, you will not be net zero emission by 2040.

I think it false to assume that Cisco cannot work with suppliers and partners across the supply chain who also prioritize renewable sources of energy as well as emissions reduction.

The goal is NET zero… Without this approach to carbon accounting, there’s no way to know who is even getting close to these goals. And the article doesn’t even mention how offsets might work to meet these goals.

So maybe we should applaud these serious efforts to deal with real problems, rather than assume they will fail? But go ahead and criticize if you want, because we all know that failure is often the key to (eventual) success.

Interesting article, what is missing is the cost of estimating the GHG emissions and further away the cost of achieving “net zero”