As my colleagues and I engage in our analysis for the Cisco Visual Networking Index, we are always on the look out for new or emerging technologies that have the potential to change network demands or user behaviors. Networks are truly organic infrastructures and many variables can have an impact on our forecast. This time around, our brainstorming sessions included a technology that is very much top of mind for many digital disrupters – Blockchain. Blockchain technology has been applied to a variety of digital transactions and it is proving to be a transformational tool for content contracts and subscriptions with enhanced security and privacy features.

According to the World Economic Forum, 10% of global gross domestic product (GDP) will be stored on blockchain platforms by 2027. A significant amount of industry buzz has also been devoted to this relatively new digital fabric (see Blockchain: The Invisible Technology That’s Changing the World).. So, I thought it might be useful to learn more about blockchain technology and why it could be a big deal.

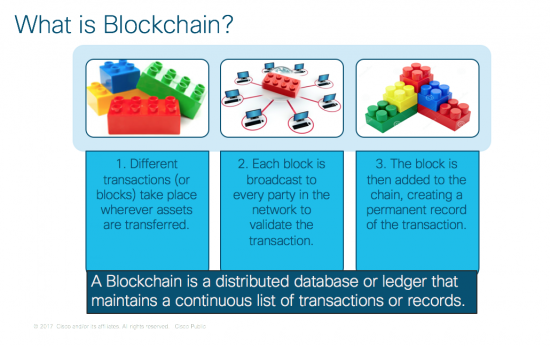

What is Blockchain?

The informal definition of blockchain is that it is a distributed ledger that maintains a constant, continuous list of records. In my mind, blockchain resembles a Lego block tower. Each transaction is like a Lego block and each block/transaction is transmitted to every party in the network. Each transaction is validated and then added to a chain, which creates a structure (like a Lego tower). The chain of transactions is then stored on multiple computers/servers, which ultimately represents a permanent irrevocable record. And that concludes the Legoanalogy. Unlike actual Lego blocks, which can be pulled apart and applied to new or different structures, blockchain records are fixed and steadfast.

How and Where is Blockchain Transforming Transactions?

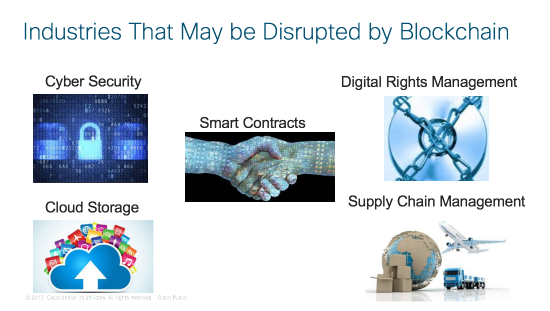

Blockchain technology has the ability to disrupt multiple technologies — cybersecurity, digital rights management, and supply chain management, just to name a few. The ability of the technology to track a transaction and maintain an immutable record will undeniably disrupt the way business is conducted today. It removes the mediator and brings the two parties involved in a transaction together with no issue of mistrust as the technology takes care of the transaction recording once the commitment criteria have been met by both parties. Transaction validation occurs once the handoff is completed on both ends (also called “Smart Contracts” or as I prefer to call it, “Programmable Contracts”).

In terms of cybersecurity, specifically DDOS attacks, there’s a major need for innovation and improvement. Cisco’s Visual Networking Index predicts that the average DDoS attack sizes are steadily increasing in number of occurrences and size. Breaches approaching 1.2 Gpbs are large enough to take most organizations completely offline and can represent up to 18% of a country’s total Internet traffic while they are active. Blockchain can help prevent DDoS attacks since the transactions/chains are saved on multiple computers or servers making it would difficult to take the entire chain down with a targeted attack on a single location.

Privacy can also be improved with blockchain. There are a few public blockchains that can be viewed by everyone in a system. However, there is a more stringent privacy option that can be used for sensitive data or files, like electronic health records (where only you, your health care professional, and insurance providers can access your relevant information, which is safe from the public view).

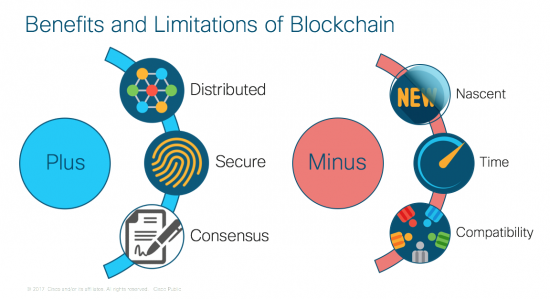

So, blockchain is a distributed system with no central authority, wherein two parties are able to exchange assets or information without any oversight or third-party intermediation. This process can reduce or even eliminate risk making the blockchain data secure, complete, consistent, timely, accurate, and widely available to those with proper authorization. The decentralized nature of blockchain makes it particularly resilient against malicious attacks. Any changes to public blockchains are transparently viewable by all parties and transactions cannot be altered or deleted. (Source: Deloitte)

But blockchain is still a very new technology and it does present quite a few challenges that need to be overcome before it can go mainstream. Because of its nascent state it is still unregulated so government regulations will also have an impact on the uptake and popularization of blockchain.

Also as transactions within a particular blockchain grow: think supply chain management with vaccines being transported from multiple countries to developing countries globally it might take longer and longer to verify transaction times. In 2016, it took an average of 43 minutes to verify a single bitcoin transaction record. By comparison, standard ATM transactions are processed almost instantaneously and reflect immediately on a financial ledger. Even interbank money transfers can be completed in seconds. As a blockchain grows, verification times might become longer, meaning more computing resources might be required to process even the smallest transaction. Small blockchains wouldn’t suffer the same problems, but this is a significant limitation of the technology in its current state.

Also, blockchain applications offer solutions that require significant changes to, or in some cases complete replacement of existing systems. In order to make the transition to blockchain technology companies must plan for this transition with care to ensure compatibility with its existing systems to maximize savings in their transaction costs but with a high capital investment upfront. Also, blockchain will require substantial buy in as it represents a completely different way of doing business with a shift to a decentralized network.

Would love to hear your thoughts on blockchain. Also stay tuned for my next blog on the impact of blockchain technology to Service Providers and to consumers.

Blockchain is definitely a worth case of analysis, tests and further study, even though presents a good security…I prefer to learn more, especially looking forward, to find out it’s possible flaws. That’s the perception of an old wolf its doings…Thank you for such interesting post and your insights.