Earlier this year Cisco completed its acquisition of imimobile, adding an enterprise-grade CPaaS platform to Cisco’s industry-leading collaboration and contact center solution portfolio. The Cisco Financial Services team welcomes imimobile’s Alex Cambell, SVP Sales at imimobile, as our blogger this week.

Changing consumer behavior and digital disruptors within the banking industry have redefined how we interact with financial service providers. We can now open new accounts, get approved for credit, transfer money to others and manage our finances, all without having to set foot in a physical branch and often within just a few clicks.

Convenience is what consumers want, but they want it without compromising on the security of their data or their financial assets. That’s why banks must realize that every interaction with customers is an opportunity to build trust and safeguard them from the latest threats.

At imimobile, we believe in giving banks the tools they need to better protect their customers whilst enhancing the overall customer experience. Here are three ways in which banking providers can do this:

Identify & reduce account takeover fraud

Account Takeover Fraud is on the rise, and the banking industry has turned to technology to combat the growing threat. Account Takeover Fraud can happen when a SIM card in the customers mobile phone is compromised with a SIM swap attempt.

SIM swap happens when fraudsters use phishing techniques to transfer a customer’s mobile phone number to a SIM in their possession. Once transferred, all communications are sent to the fraudster’s device, allowing them to take over customer accounts to access data and transfer funds.

Technology solutions can help banks and other financial institutions to detect suspicious SIM swap activity. They can identify the risk of SIM swap fraud based on location, device type, customer behavior and other factors. Platforms such as imiconnect can use mobile network information to monitor a customer’s SIM for the risks above. Then through integrations with other business systems and workflows, the platform can trigger corrective actions based on the fraud risk-level of a SIM swap, e.g., blocking transactions, locking accounts or sending customer communications.

Banks looking to safeguard customers from SIM swap fraud, should consider investing in a platform that can monitor suspicious activity and automate follow-up actions to protect customers.

Build robust authentication processes

Regulations around authentication processes are constantly changing, and often differ from country to country. Across the EU, the Financial Conduct Authority recently provided a further six-month extension to a deadline which forces financial institutions to strengthen their customer authentication rules as many organizations were struggling to implement the appropriate processes in time.

So, what do strong customer authentication processes look like? Regulations such as PSD2 define strong customer authentication as an authentication based on the use of two or more elements categorized as the following:

- Knowledge – something only the user knows such as a password or a pin

- Possession – something only the user possesses such as security tokens

- Inherence – something that is part of what the user is such as fingerprint scanners or voice recognition technology.

However, banks and other financial institutions often struggle to implement these robust authentication processes whilst maintaining a seamless experience for customers.

Banks should add a layer of security to customer accounts with one-time passwords and two-factor authentication. They can also use technology platforms to unify data sources and conduct third-party checks to create an extensive profile of every customer. It’s important for them to work with a trusted technology partner who has extensive experience implementing these types of solutions with large retail banks.

Use the latest digital channels to build trust

Customer trust is essential to increasing customer engagement, particularly for financial services providers. It’s been reported that SMS phishing has increased by more than 300% since the start of the pandemic and 87% customers won’t answer a call unless they recognize the number. However, there are a new wave of digital channels that banks can use to improve trust, security and brand recognition.

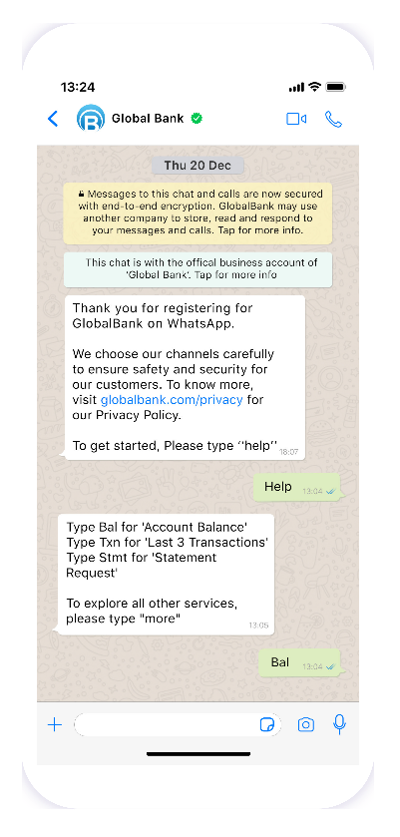

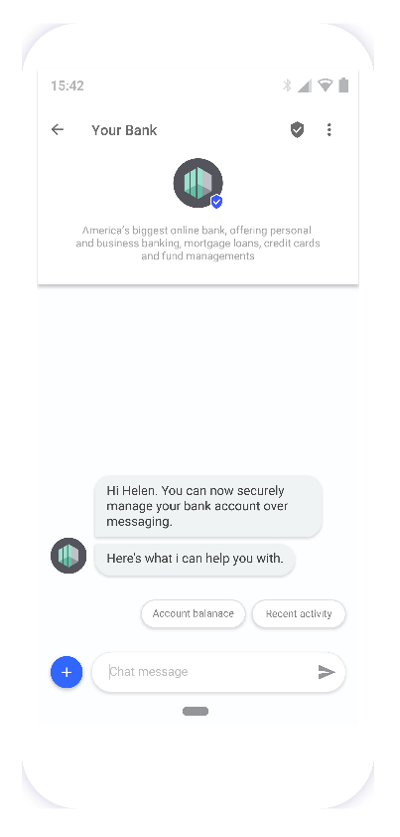

Channels like Apple Business Chat and WhatsApp Business offer the ability for brands to add company logos, descriptions, contact information and ‘green tick’ verification badges to build a verified business profile that customers can trust. They also offer end-to-end encryption to ensure that customer interactions remain private.

Technology giant Google also offers verified communications over two channels – Verified SMS and Verified Calls. Both channels add a layer of authentication to standard communication channels that businesses already use every day. Verified SMS makes SMS messaging safer and more trustworthy by adding sender verification, link previews and branding to messages. Verified Calls displays a brand’s name, logo, reason for calling and a verification symbol when a call is made.

Banking providers should consider implementing these new channels in order to build trust with their customers, reduce the chance of fraud as well as improving the overall customer experience.

Every interaction builds trust. At imimobile, we help global financial institutions such as Barclays, Lloyds Bank and RBS create connected banking experiences that build lasting customer relationships. Check out our banking solutions here, at Cisco’s financial services website, or get in touch with one of our experts today.

Great insights Alex and great as well to have IMImobile’s team and solutions as part of Cisco’s industry-leading collaboration and contact center portfolio!