By Robert Mahowald, IDC Group Vice President

IDC recently surveyed more than 6,159 executive-level IT and LOB decision makers in 31 countries to find out their future plans and current state of cloud adoption. What we discovered is pretty remarkable.

According to IDC’s CloudView Survey 2016, 78% of organizations are already using or planning to implement some form of cloud services, up from 60% in last year’s survey. Sixty-six percent of organizations we surveyed are using or planning to implement private clouds. But respondents pointed to hybrid cloud — a strategy for operating in a mix of public and private cloud, provider and customer-based environments — as their dominant operational model, at 73% of all organizations surveyed.

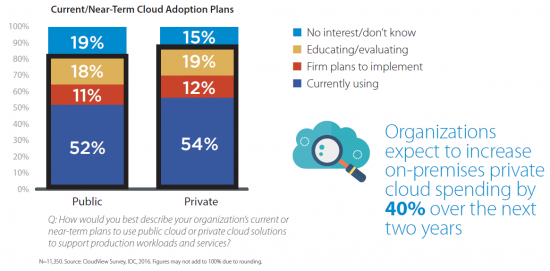

Moreover, organizations intend to invest more money in hybrid clouds. Over the next 2 years, we expect a 30% increase in the number of cloud users planning to allocate funds to more than one type of cloud deployment as part of a hybrid cloud strategy. It’s important to note that future budget allocations for provider-based cloud plans grow primarily at the expense of spending for traditional in-house IT. This means that organizations are focusing on sorting out what types of workloads are best suited for private clouds (re-platformed, virtualized and/or containerized to run in the corporate datacenter) versus public clouds (running at a provider’s site). In general, sustained workloads requiring control and compliance, such as financial planning applications, tend to be allocated to private clouds, while elastic workloads such as analytics, or eCommerce can go to public cloud providers for quicker ramp-up and scalable services. Nonetheless, organizations expect to increase on-premises private cloud spending by 40% over the next two years.

Hybrid cloud growth also means that organizations are expecting greater returns from their cloud investments on strategic business outcomes. For example, more than half of all organizations expect to increase revenues from their use of cloud services. However, only 31% of organizations in our survey had repeatable, managed, or optimized cloud strategies, and 22% had no cloud strategy at all. Nearly 50% had a 2-year goal to achieve “Optimized” maturity, the highest level of sourcing and management in IDC’s Cloud Maturity Model. But only 3% of firms currently have that fully-optimized cloud strategy. Obstacles to achieving greater cloud maturity include skill gaps, legacy siloed organization structures and IT/LOB misalignment. Clearly there is significant room for improvement, which perhaps is why 89% of organizations think it’s important to work with their major incumbent provider to carry current operations into the cloud.

IDC research indicates that these expectations of cloud adoption are grounded in tangible benefits. Organizations we’ve studied are now realizing $3 million in revenues and $1million in reduced costs per cloud application deployed on a yearly basis. Most respondents expect to migrate data between public and private clouds, and they have high security and policy requirements. These IT executives also expect to act as IT service brokers and want solutions that support their requirements.

Indeed, IDC foresees the emergence of “Provider-Based Cloud,” in which trusted IT infrastructure vendors become the cloud providers of choice. IDC sees a growing potential for IT incumbents to deliver feature-rich cloud services fully managed by the enterprise, with features such as mobile asset management, directory integration, and customer-managed encryption keys.

Additionally, what IDC sees as the “second wave” of cloud adoption continues to advance. The first wave was tied to metrics such as improved service-level agreements (SLAs) and lower costs, but now organizations view cloud as a platform that can help them drive innovation and digital transformation. In fact, this study shows that as companies achieve greater levels of cloud maturity, business benefits increased. The more mature organizations have greater revenue and are able to more strategically allocate their IT budgets to keep more focus on innovation and less on activities necessary to “keep the lights on.” However, the second wave has not reached all IT buyers yet. There are still organizations out there who resist cloud deployment, citing security concerns (48%) and high costs (26%) as the top two reasons for their stagnation, according to IDC CloudView.

For more information and guidance on cloud adoption, I invite you to read the IDC InfoBrief “Cloud Going Mainstream. All Are Trying, Some Are Benefiting; Few Are Maximizing Value” sponsored by Cisco. Cisco has also made many of these market research findings actionable by developing the Cisco Business Cloud Advisor (BCA) framework enabled by IDC. Begin to explore the possibilities by completing a brief survey.

Author Bio

Robert Mahowald is a Group Vice President at IDC and leads IDC’s Applications team, the Cloud Software team, and co-leads IDC’s Cloud Services: Global Overview program. In his roles, Robert advises clients on key trends and opportunities in the changing world of software creation and delivery in the age of cloud computing. An experienced speaker, Mr. Mahowald is well-known as a subject matter expert in the areas of SaaS, IT cloud services and software application delivery. He has been a featured lecturer at various executive events, industry seminars and conferences such as InternetWorld, and on such television programs as CNBC and CNET TV. Mr. Mahowald’s research and commentary has appeared in trade journals and publications including The Wall Street Journal, USA Today, The New York Times, and Investor’s Business Daily.

Robert Mahowald is a Group Vice President at IDC and leads IDC’s Applications team, the Cloud Software team, and co-leads IDC’s Cloud Services: Global Overview program. In his roles, Robert advises clients on key trends and opportunities in the changing world of software creation and delivery in the age of cloud computing. An experienced speaker, Mr. Mahowald is well-known as a subject matter expert in the areas of SaaS, IT cloud services and software application delivery. He has been a featured lecturer at various executive events, industry seminars and conferences such as InternetWorld, and on such television programs as CNBC and CNET TV. Mr. Mahowald’s research and commentary has appeared in trade journals and publications including The Wall Street Journal, USA Today, The New York Times, and Investor’s Business Daily.

There’s no doubt that the way to go is through a totally Cloud adoption. Very good blog post.