I fondly recall in the not-too-distant past, Bank of America radio commercials boasting about its branch network. In the lighthearted radio commercial, the person was giving directions and using the location of Bank of America branches as where to turn. This promoted how convenient Bank of America branches were in most places, almost on every street corner like Starbucks. Today those same directions might only take you from one city to the next.

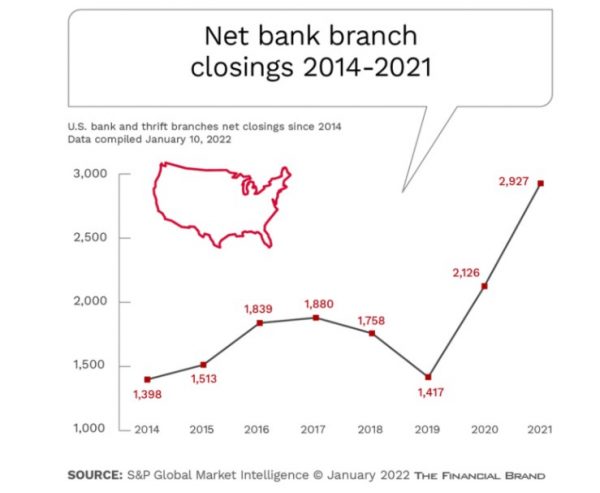

The size of your branch network used to be a valuable measuring stick. In 2009 when the closing of branches trend began the U.S. had nearly 100,000 branches. At the beginning of 2021 there were just over 80,000. In 2021 on net, U.S. banks shuttered 2,927 branches, according to S&P Global Market Intelligence data. Last year banks closed nearly 4,000 branches and opened more than 1,000 branches.

However, if branches were truly going the way of dinosaur, then why would JPMorgan Chase open 169 locations in 2021? Yes, JPMorgan Chase was also the sixth-biggest net branch closer in 2021. Branches are evolving as they are no longer the transaction hubs they once were. Instead, research shows that a majority of consumers still prefer branches for more complex financial needs and that small businesses prefer human interaction. Financial institutions have to rethink of the utilization of the branch and overall channel delivery strategy.

Branches are a valuable component of your brand, a physical and visible symbol of safety and security of your money. Yes, everyone knows that their money is not located in their local branch, but they know that if a problem arises or they want advice and guidance a real live person is within reach. According to PwC’s 2021 Digital Banking Consumer Survey, two in three customers find branches to be meaningful channel to interact with their bank and 35% say that they would not use a bank that doesn’t have a nearby location. And yet all kinds of ideas and gimmicks are being tried to make branches more inviting: community centers, yoga studios, or coffee bars.

Commerce disruptor Amazon has found value in operating physical stores, financial institutions should be able as well. Branches should focus on more complex financial services and relationship management. This strategy allows customers to go, see, touch, question and understand the products by speaking with representatives. In essence it is about technology that enables and improves experience, execution, and optimization of the physical branch.

This is where Cisco technology can help.

Empower the branch

Improve the customer experience and enhance servicing by onboarding arriving customers with secure Wi-Fi connectivity and personalized services – such as welcome messages, branch details, and customized digital signage. Branches must be adaptive to serve evolving customer expectations. Provide analytics with insights into branch activity. This insight can be used to trigger dynamic and informed branch engagement through mobile applications using available mobility APIs.

Offer connected financial journeys

Consumers prefer digital channels when researching financial products. However, as mentioned in the PwC Digital Banking Survey 33% still prefer the branch for certain activities. Financial institutions can leverage the flexible, secure connectivity of Cisco to deliver intelligence from on-premises and software-as-a-service (SaaS) solutions that connect the digital and physical customer experience. The result is a desirable integrated omni-channel experience where branch staff have insight into customers’ needs.

Branch staff can also deliver the full range of financial services through high-definition video to provide advice virtually. Improve the productivity of specialists and optimize staffing, all while meeting the customer’s wide-ranging needs.

Optimize branch operations

Rethink how to execute the branch space. Use sensor and location data to provide customer insights to staff in real time, improving service delivery, staff productivity, and operational awareness. Branch space can become more adaptive through secure mobility that enables staff to better serve customers in any area of the branch.

Financial institutions need a new foundational branch infrastructure that can be deployed faster, with services that can be enabled cost-effectively and at scale. With Cisco, an institution’s branches can be brought online faster, at a lower cost, and can be managed more efficiently, improving competitiveness and overall branch profitability. No latte needed.

Check out the Financial Services webpage for more information.